Teaching Machines the Art of Regret¶

Every model makes predictions. Some are close; some miss badly. Mean Squared Error (MSE) is the training objective that tells a model how much it should regret its mistakes — and by minimising it, the model learns to improve.

Learning Objectives¶

Why MSE Matters in Business and ML¶

Business context

Imagine you run a coffee chain and your demand-forecasting model predicts daily cups sold.

| Scenario | Actual | Predicted | Impact |

|---|---|---|---|

| Close miss | 500 | 480 | Minor over-order ☕ |

| Big miss | 500 | 50 | Catastrophic shortage 😱 |

A metric that treats both misses equally would suggest the big miss is fine if other stores also over-predicted. Squaring the error ensures the catastrophic miss dominates the average — which is exactly the behaviour you want when large mistakes are disproportionately costly.

In machine learning, MSE is also the loss surface that gradient descent descends to fit the model. Understanding it is therefore not just about evaluation — it is about understanding how a linear model learns.

Where MSE sits in the regression workflow

This notebook covers the orange box — defining the training objective. Optimisation details are in gradients.ipynb and ols.ipynb; evaluation metrics are in regression_metrics.ipynb.

The MSE Formula¶

Residuals¶

For observation , the residual is the gap between the true label and the prediction:

\color{#1f77b4}{\text{blue} = \text{actual}}

,

\color{#ff7f0e}{\text{orange} = \text{predicted}},

\color{#d62728}{\text{red} = \text{residual}}Mean Squared Error¶

MSE averages the squared residuals over all training examples:

As a training objective (also written as cost function ):

The is a convention: it cancels with the exponent when you differentiate, keeping derivative expressions clean. The (or ) scaling does not change which minimises .

RMSE¶

MSE is in squared units (e.g., sales² if you predict sales). Root Mean Squared Error brings the units back:

RMSE is easier to communicate: “our model is off by about 19 cups per day on average.”

Visual Intuition: What MSE Measures¶

Geometrically, MSE sums the area of squares whose sides are the vertical gaps between each data point and the fitted line. The line that minimises the total area is the OLS solution.

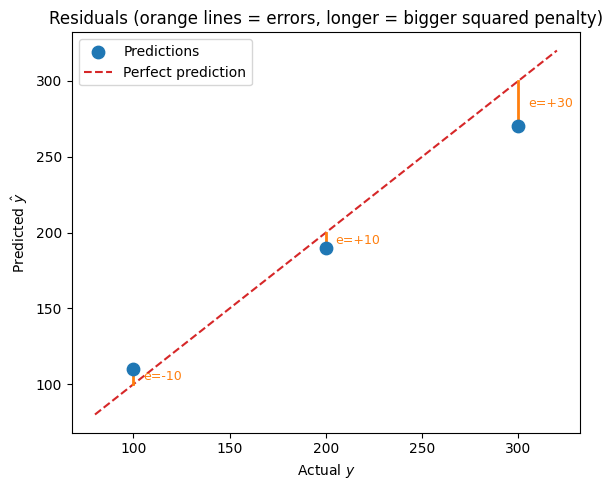

Worked Example: Predicting Sales¶

| Observation | Actual | Predicted | Residual | Squared residual |

|---|---|---|---|---|

| 1 | 100 | 110 | −10 | 100 |

| 2 | 200 | 190 | +10 | 100 |

| 3 | 300 | 270 | +30 | 900 |

Observation 3 contributes 900 to the sum — nine times more than observations 1 and 2 combined. That is the heavy penalty for large mistakes at work.

Code: Computing MSE and RMSE¶

import numpy as np

from sklearn.metrics import mean_squared_error

y_true = np.array([100, 200, 300])

y_pred = np.array([110, 190, 270])

mse = mean_squared_error(y_true, y_pred)

rmse = np.sqrt(mse)

residuals = y_true - y_pred

squared_residuals = residuals ** 2

print(f"Residuals: {residuals}")

print(f"Squared residuals: {squared_residuals}")

print(f"MSE: {mse:.2f}")

print(f"RMSE: {rmse:.2f}")Residuals: [-10 10 30]

Squared residuals: [100 100 900]

MSE: 366.67

RMSE: 19.15

Visualising the residuals¶

%matplotlib inline

import numpy as np

import matplotlib.pyplot as plt

y_actual = np.array([100, 200, 300])

y_pred = np.array([110, 190, 270])

fig, ax = plt.subplots(figsize=(6, 5))

ax.scatter(y_actual, y_pred, color='#1f77b4', s=80, zorder=5, label='Predictions')

ax.plot([80, 320], [80, 320], color='#d62728', linestyle='--', lw=1.5, label='Perfect prediction')

for ya, yp in zip(y_actual, y_pred):

ax.plot([ya, ya], [ya, yp], color='#ff7f0e', lw=2)

ax.annotate(f'e={ya-yp:+g}', xy=(ya, (ya+yp)/2), xytext=(ya+5, (ya+yp)/2),

fontsize=9, color='#ff7f0e', va='center')

ax.set_xlabel('Actual $y$')

ax.set_ylabel('Predicted $\\hat{y}$')

ax.set_title('Residuals (orange lines = errors, longer = bigger squared penalty)')

ax.legend()

plt.tight_layout()

plt.show()

MSE as a Training Objective¶

When training a linear model, the goal is to find the parameter vector that minimises :

In matrix–vector form (the design matrix , target vector ):

Setting the gradient to zero and solving yields the Normal Equations:

Gradient derivation (reference)

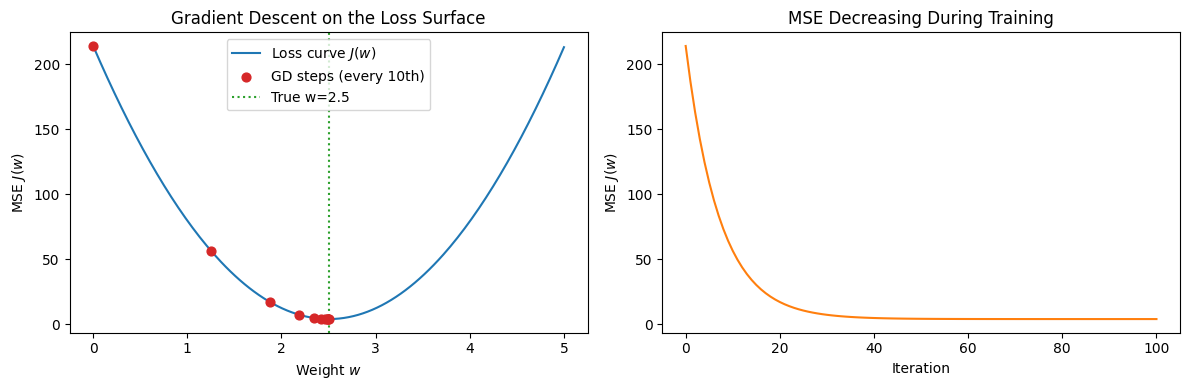

The gradient descent update rule (preview)¶

Rather than solving the Normal Equations directly, gradient descent iteratively steps toward lower :

where is the learning rate. The algorithm repeats until is below a convergence threshold:

theta, theta_prev = random_initialization()

while norm(theta - theta_prev) > convergence_threshold:

theta_prev = theta

theta = theta_prev - step_size * gradient(theta_prev)Code: Gradient Descent Descending the Loss Curve¶

%matplotlib inline

import numpy as np

import matplotlib.pyplot as plt

np.random.seed(0)

X = np.linspace(0, 10, 100)

true_w = 2.5

y = true_w * X + np.random.normal(0, 2, size=X.shape)

def compute_loss(w):

return np.mean((y - w * X) ** 2)

def compute_gradient(w):

return -2 * np.mean(X * (y - w * X))

w_values = np.linspace(0, 5, 200)

loss_vals = [compute_loss(w) for w in w_values]

w_cur = 0.0

lr = 0.001

w_hist = [w_cur]

loss_hist = [compute_loss(w_cur)]

for _ in range(100):

w_cur -= lr * compute_gradient(w_cur)

w_hist.append(w_cur)

loss_hist.append(compute_loss(w_cur))

fig, axes = plt.subplots(1, 2, figsize=(12, 4))

axes[0].plot(w_values, loss_vals, label='Loss curve $J(w)$', color='#1f77b4')

axes[0].scatter(w_hist[::10], loss_hist[::10], color='#d62728', s=40, zorder=5, label='GD steps (every 10th)')

axes[0].axvline(x=true_w, color='#2ca02c', linestyle=':', lw=1.5, label=f'True w={true_w}')

axes[0].set_xlabel('Weight $w$')

axes[0].set_ylabel('MSE $J(w)$')

axes[0].set_title('Gradient Descent on the Loss Surface')

axes[0].legend()

axes[1].plot(loss_hist, color='#ff7f0e')

axes[1].set_xlabel('Iteration')

axes[1].set_ylabel('MSE $J(w)$')

axes[1].set_title('MSE Decreasing During Training')

plt.tight_layout()

plt.show()

print(f"Final learned w = {w_hist[-1]:.4f} (true = {true_w})")

Final learned w = 2.5003 (true = 2.5)

Interactive: Compute MSE in Your Browser¶

Try changing the predicted values below and watch how MSE and RMSE respond.

MSE vs Other Regression Metrics¶

| Metric | Formula | Units | Penalises big errors? | Use when |

|---|---|---|---|---|

| MSE | target² | Heavily | Training objective; large-error-sensitive tasks | |

| RMSE | target | Heavily | Communicating error magnitude to stakeholders | |

| MAE | $\frac{1}{n}\sum | e_i | $ | target |

| R² | — | N/A | Explaining variance accounted for by the model |

Common pitfalls¶

| Pitfall | Why it matters |

|---|---|

| Comparing MSE across datasets with different scales | MSE grows with the magnitude of — a higher MSE does not always mean a worse model |

| Reporting MSE without RMSE | MSE is in squared units, making it hard to interpret in meetings |

| Achieving zero MSE on training data | Perfect training fit usually means overfitting — the model has memorised the data |

| Ignoring residual plots | MSE gives one number; residual patterns reveal bias, heteroscedasticity, and missed non-linearity |

Code: Animated Residuals (Fitting Process)¶

%matplotlib inline

import matplotlib.pyplot as plt

import numpy as np

from matplotlib.animation import FuncAnimation, PillowWriter

from IPython.display import Image

np.random.seed(42)

x_data = np.linspace(0, 10, 20)

y_data = (2 * x_data + 1) + np.random.normal(0, 2, 20)

fig, ax = plt.subplots(figsize=(7, 5))

ax.set_xlim(0, 10)

ax.set_ylim(0, 25)

ax.scatter(x_data, y_data, color='#1f77b4', zorder=5, label='Data points')

line, = ax.plot([], [], 'r-', lw=2, label='Model line')

error_lines = [ax.plot([], [], color='#ff7f0e', lw=1.2, linestyle='--')[0] for _ in range(len(x_data))]

loss_text = ax.text(0.02, 0.95, '', transform=ax.transAxes, va='top', fontsize=9)

def init():

line.set_data([], [])

for el in error_lines:

el.set_data([], [])

loss_text.set_text('')

return (line, *error_lines, loss_text)

def animate(i):

slope = 0.5 + i * 0.1

intercept = 0.0 + i * 0.2

y_pred = slope * x_data + intercept

mse_val = np.mean((y_data - y_pred) ** 2)

line.set_data(x_data, y_pred)

for j, el in enumerate(error_lines):

el.set_data([x_data[j], x_data[j]], [y_data[j], y_pred[j]])

loss_text.set_text(f'MSE = {mse_val:.1f}')

return (line, *error_lines, loss_text)

ani = FuncAnimation(fig, animate, frames=np.arange(25), init_func=init, interval=300, blit=True)

ax.legend(loc='upper left', fontsize=8)

ax.set_title('Residuals as the model line sweeps (orange = errors)')

plt.close(fig) # prevent a static frame appearing alongside the GIF

ani.save('squared_error.gif', writer=PillowWriter(fps=8))

Image(filename='squared_error.gif')

Guided Practice¶

Why does MSE penalise large errors more heavily than MAE?¶

What does an MSE of zero on the training set indicate?¶

Why does the MSE cost function often include a $\frac{1}{2}$ factor?¶

Exercises¶

Exercise 1 — Manual MSE Calculation¶

You are forecasting next month’s revenue for four stores:

| Store | Actual ($) | Predicted ($) |

|---|---|---|

| A | 50 000 | 48 000 |

| B | 75 000 | 80 000 |

| C | 60 000 | 65 000 |

| D | 90 000 | 100 000 |

Compute MSE and RMSE.

Which store has the largest squared error? What business action might that trigger?

Would you prefer to report MSE or RMSE to your manager, and why?

import numpy as np

y_true = np.array([50000, 75000, 60000, 90000])

y_pred = np.array([48000, 80000, 65000, 100000])

# Your code here

# mse = ...

# rmse = ...Show solution

import numpy as np

y_true = np.array([50000, 75000, 60000, 90000])

y_pred = np.array([48000, 80000, 65000, 100000])

residuals = y_true - y_pred

squared_residuals = residuals ** 2

mse = np.mean(squared_residuals)

rmse = np.sqrt(mse)

stores = ['A', 'B', 'C', 'D']

for s, sq in zip(stores, squared_residuals):

print(f"Store {s}: squared error = {sq:>15,.0f}")

print(f"\nMSE = {mse:>15,.0f}")

print(f"RMSE = {rmse:>15,.2f} (on average off by ~${rmse:,.0f})")Answers:

MSE ≈ 33,750,000; RMSE ≈ $5,811.

Store D has the largest squared error (100,000²= 10⁹ × 10⁻⁴ → 10,000² = 100,000,000). That 10 % miss on the largest store dominates.

Report RMSE to a manager — “we are off by about $5,800 per store on average” is much more interpretable than a number in squared dollars.

Exercise 2 — Effect of an Outlier¶

Add a fifth store (E) with actual = 100 000, predicted = 200 000 (a catastrophic 100 k miss).

How much does the MSE change?

How does the same outlier affect MAE?

What does this reveal about choosing metrics for a business problem?

import numpy as np

y_true_ext = np.array([50000, 75000, 60000, 90000, 100000])

y_pred_ext = np.array([48000, 80000, 65000, 100000, 200000])

# Compute MSE and MAE with and without the outlier, compare

# Your code hereShow solution

import numpy as np

y_true_base = np.array([50000, 75000, 60000, 90000])

y_pred_base = np.array([48000, 80000, 65000, 100000])

y_true_ext = np.array([50000, 75000, 60000, 90000, 100000])

y_pred_ext = np.array([48000, 80000, 65000, 100000, 200000])

def report(yt, yp, label):

mse = np.mean((yt - yp)**2)

mae = np.mean(np.abs(yt - yp))

print(f"{label}: MSE={mse:>18,.0f} MAE={mae:>8,.0f}")

report(y_true_base, y_pred_base, "4 stores (no outlier) ")

report(y_true_ext, y_pred_ext, "5 stores (with outlier)")The single 100 k outlier inflates MSE massively but MAE increases much more moderately. This illustrates why MSE-based training makes the model very sensitive to outliers — which is either a feature or a bug depending on your business context.

Summary¶

Key takeaways

| Concept | One-line summary |

|---|---|

| Residual | The gap between an observed value and its prediction: |

| MSE | Average squared residual: |

| Why square? | Eliminates sign; punishes large errors; smooth for calculus |

| RMSE | — same units as target, easier to explain |

| Training objective | We choose to minimise |

| Normal Equations | Closed-form solution: |

| Sensitivity | MSE is heavily influenced by outliers; MAE is more robust |

Next Steps¶

You now know what MSE measures and why it is the right training objective for ordinary least-squares regression. The next notebooks build on this foundation:

regression_metrics.ipynb — full held-out evaluation: RMSE, MAE, R², adjusted R², residual diagnostics.

gradients.ipynb — how gradient descent uses $\nabla J$ to iteratively minimise MSE step by step.

ols.ipynb — the closed-form Normal Equations solution derived in full.