Logistic Regression¶

Learning objectives

By the end of this notebook you will be able to:

Explain why the sigmoid maps a linear score to a probability.

Derive and interpret the binary cross-entropy (BCE) loss.

Connect MLE to the BCE objective and MAP to L2-regularised BCE.

Interpret weights as log-odds and exponentiated weights as odds ratios.

Implement

LogisticRegressionfrom scratch with gradient descent and L2 regularisation.Extend logistic regression to K classes via softmax regression.

Implement

SoftmaxRegressionfrom scratch and visualise decision boundaries.Identify common pitfalls: class imbalance, feature scaling, and separability.

Apply logistic regression to a real classification problem end-to-end.

Business hook — Will this customer churn?¶

A telecoms company wants to know: given a customer’s usage pattern, will they cancel their subscription next month? This is a binary question — yes or no — and the business needs a probability, not just a label. A 90 % churn probability triggers a retention call; 10 % does not.

Linear regression would predict a raw number that can exceed 1 or drop below 0 — neither is a valid probability. Logistic regression solves this with a single non-linear squashing function: the sigmoid.

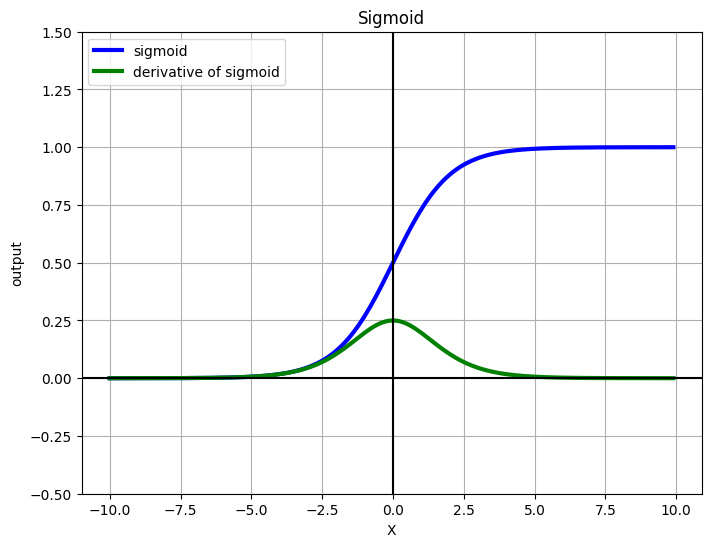

1. The Sigmoid Function¶

The sigmoid function squashes any real number to :

where is the linear score.

Key properties:

| Property | Value |

|---|---|

| Range | — valid probability |

| 0.5 — decision boundary | |

| as | high score → class 1 |

| as | low score → class 0 |

| Derivative | — elegant! |

The derivative being expressible in terms of itself makes backpropagation (and analytical gradient derivation) clean.

%matplotlib inline

from __future__ import division

import numpy as np

import matplotlib.pyplot as plt

def sigmoid(x):

return 1 / (1 + np.exp(-x))

def grad_sigmoid(x):

return sigmoid(x) * (1 - sigmoid(x))

X = np.arange(-10, 10, 0.1)

fig = plt.figure(figsize=(8, 6))

plt.plot(X, sigmoid(X), label='sigmoid', c='blue', linewidth=3)

plt.plot(X, grad_sigmoid(X), label='derivative of sigmoid', c='green', linewidth=3)

plt.legend(loc='upper left')

plt.xlabel('X')

plt.grid(True)

plt.ylim([-0.5, 1.5])

plt.ylabel('output')

plt.title('Sigmoid')

plt.axhline(y=0, color='k')

plt.axvline(x=0, color='k')

plt.show()

2. The Decision Boundary¶

The model predicts class 1 when , which happens when :

The decision boundary is the hyperplane . In 2D this is a line; in dimensions it is a -dimensional hyperplane.

Non-linear boundaries are possible by adding polynomial or interaction features before fitting — logistic regression itself is always a linear classifier in the transformed feature space.

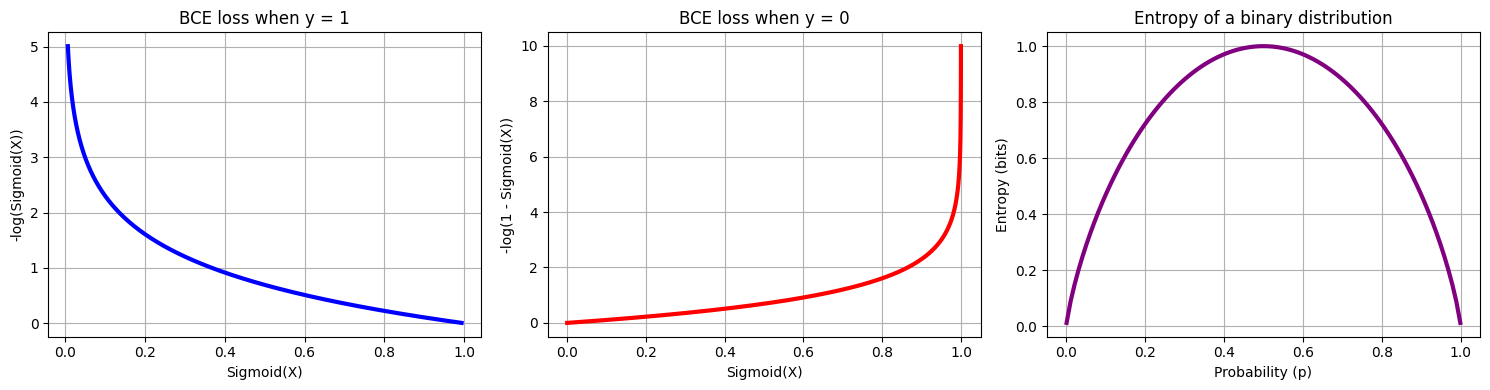

3. Binary Cross-Entropy Loss¶

Why not use MSE? MSE applied to a sigmoid output creates a non-convex loss surface — many local minima, poor gradients near 0 and 1.

Binary cross-entropy (BCE) is the correct loss for binary classification:

When : loss — penalises low predicted probability

When : loss — penalises high predicted probability

The combined loss is convex when composed with the sigmoid, guaranteeing a unique global minimum.

Entropy and log-loss. Shannon entropy measures uncertainty of a distribution. Log-loss measures how far our predicted distribution is from the true labels — it equals the cross-entropy between the empirical distribution (labels) and the model’s predicted distribution.

%matplotlib inline

import numpy as np

import matplotlib.pyplot as plt

def sigmoid(x):

return 1 / (1 + np.exp(-x))

def entropy(p):

p = np.clip(p, 1e-10, 1 - 1e-10)

return -p * np.log2(p) - (1 - p) * np.log2(1 - p)

def log_loss(y_true, y_pred):

y_pred = np.clip(y_pred, 1e-10, 1 - 1e-10)

return - (y_true * np.log(y_pred) + (1 - y_true) * np.log(1 - y_pred))

fig, axes = plt.subplots(1, 3, figsize=(15, 4))

X = np.arange(-5, 5, 0.01)

axes[0].plot(sigmoid(X), -np.log(sigmoid(X)), c='blue', linewidth=3)

axes[0].set_xlabel('Sigmoid(X)')

axes[0].set_ylabel('-log(Sigmoid(X))')

axes[0].set_title('BCE loss when y = 1')

axes[0].grid(True)

X = np.arange(-10, 10, 0.01)

axes[1].plot(sigmoid(X), -np.log(1 - sigmoid(X)), c='red', linewidth=3)

axes[1].set_xlabel('Sigmoid(X)')

axes[1].set_ylabel('-log(1 - Sigmoid(X))')

axes[1].set_title('BCE loss when y = 0')

axes[1].grid(True)

p_vals = np.linspace(0.001, 0.999, 100)

axes[2].plot(p_vals, entropy(p_vals), c='purple', linewidth=3)

axes[2].set_xlabel('Probability (p)')

axes[2].set_ylabel('Entropy (bits)')

axes[2].set_title('Entropy of a binary distribution')

axes[2].grid(True)

plt.tight_layout()

plt.show()

4. Gradient of the BCE Loss¶

With , the gradient of BCE with respect to is:

This has the same form as the linear regression gradient — the model error is back-propagated through the features. The sigmoid derivative cancels cleanly with the BCE terms.

Gradient update rule (same as previous notebooks):

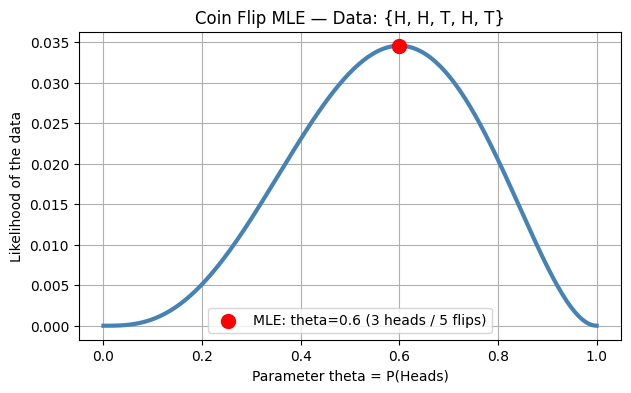

5. MLE vs MAP — From Probability to Regularisation¶

Maximum Likelihood Estimation (MLE) finds that maximises the probability of observing the training labels:

Taking the negative log gives exactly the BCE loss — MLE = unregularised BCE minimisation.

Maximum A Posteriori (MAP) adds a prior over . With a Gaussian prior :

MAP + Gaussian prior = L2-regularised BCE.

| Method | Objective | sklearn C | Behaviour |

|---|---|---|---|

| MLE | Pure BCE | Unregularised, can overfit | |

| MAP (Gaussian prior) | BCE + L2 | Shrinks weights, reduces variance | |

| MAP (Laplace prior) | BCE + L1 | — | Sparse weights, feature selection |

%matplotlib inline

import numpy as np

import matplotlib.pyplot as plt

# Coin flip MLE: dataset {H, H, T, H, T} — theta = P(H)

coin_likelihood = lambda theta: theta*theta*(1-theta)*theta*(1-theta)

theta_vals = np.linspace(0, 1, 200)

plt.figure(figsize=(7, 4))

plt.plot(theta_vals, coin_likelihood(theta_vals), linewidth=3, c='steelblue')

plt.scatter([0.6], [coin_likelihood(0.6)], color='red', s=100, zorder=5,

label='MLE: theta=0.6 (3 heads / 5 flips)')

plt.xlabel('Parameter theta = P(Heads)')

plt.ylabel('Likelihood of the data')

plt.title('Coin Flip MLE — Data: {H, H, T, H, T}')

plt.legend()

plt.grid(True)

plt.show()

print('MLE estimate: theta = 3/5 =', 3/5, '(number of heads / total flips)')

MLE estimate: theta = 3/5 = 0.6 (number of heads / total flips)

6. Weight Interpretation — Log-Odds and Odds Ratios¶

The log-odds (logit) of the model’s prediction is:

This is linear in the features. Each coefficient is the change in log-odds per unit increase in (all else held constant).

Odds ratio interpretation:

: one unit increase in doubles the odds of class 1.

: one unit increase halves the odds.

: has no effect.

Important: always standardise features before interpreting magnitudes (coefficients only compare across features when features are on the same scale).

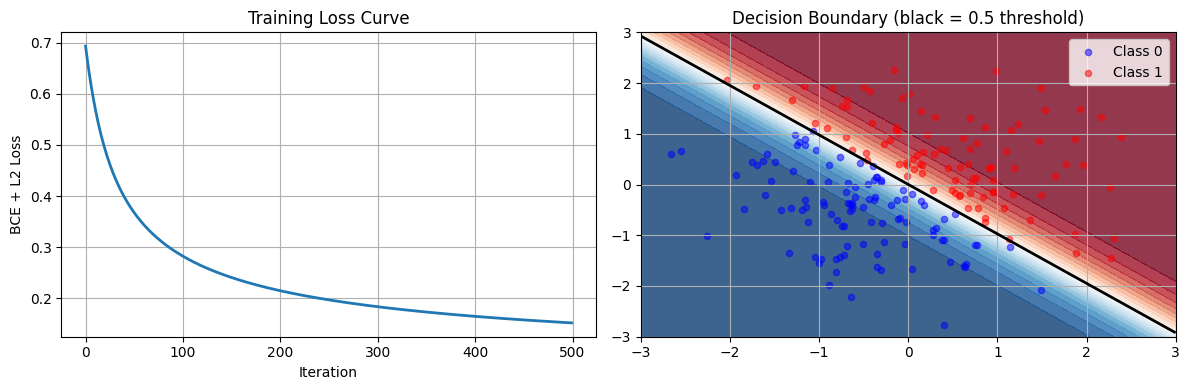

7. Logistic Regression from Scratch¶

The implementation below follows the GD loop from Chapter 6 — only the loss function and gradient change from linear regression.

%matplotlib inline

import numpy as np

import matplotlib.pyplot as plt

class LogisticRegression:

def __init__(self, learning_rate=0.01, n_iterations=1000, lambda_reg=0.01):

self.learning_rate = learning_rate

self.n_iterations = n_iterations

self.lambda_reg = lambda_reg

self.weights = None

self.bias = None

self.losses = []

def sigmoid(self, z):

return 1 / (1 + np.exp(-z))

def compute_loss(self, X, y, y_pred):

N = len(y)

cross_entropy = -np.mean(y * np.log(y_pred + 1e-15) + (1 - y) * np.log(1 - y_pred + 1e-15))

l2_penalty = (self.lambda_reg / (2 * N)) * np.sum(self.weights ** 2)

return cross_entropy + l2_penalty

def fit(self, X, y):

n_samples, n_features = X.shape

self.weights = np.zeros(n_features)

self.bias = 0

for _ in range(self.n_iterations):

linear_model = np.dot(X, self.weights) + self.bias

y_pred = self.sigmoid(linear_model)

loss = self.compute_loss(X, y, y_pred)

self.losses.append(loss)

dw = (1 / n_samples) * np.dot(X.T, (y_pred - y)) + (self.lambda_reg / n_samples) * self.weights

db = (1 / n_samples) * np.sum(y_pred - y)

self.weights -= self.learning_rate * dw

self.bias -= self.learning_rate * db

def predict_proba(self, X):

linear_model = np.dot(X, self.weights) + self.bias

return self.sigmoid(linear_model)

def predict(self, X, threshold=0.5):

return (self.predict_proba(X) >= threshold).astype(int)

np.random.seed(0)

X = np.random.randn(200, 2)

y = (X[:, 0] + X[:, 1] > 0).astype(int)

model = LogisticRegression(learning_rate=0.1, n_iterations=500, lambda_reg=0.1)

model.fit(X, y)

y_pred = model.predict(X)

accuracy = np.mean(y_pred == y)

print(f'Training accuracy: {accuracy:.4f}')

print(f'Final loss: {model.losses[-1]:.4f}')

fig, axes = plt.subplots(1, 2, figsize=(12, 4))

axes[0].plot(model.losses, linewidth=2)

axes[0].set_xlabel('Iteration')

axes[0].set_ylabel('BCE + L2 Loss')

axes[0].set_title('Training Loss Curve')

axes[0].grid(True)

xx, yy = np.meshgrid(np.linspace(-3, 3, 200), np.linspace(-3, 3, 200))

Z = model.predict_proba(np.c_[xx.ravel(), yy.ravel()]).reshape(xx.shape)

axes[1].contourf(xx, yy, Z, levels=20, cmap='RdBu_r', alpha=0.8)

axes[1].scatter(X[y==0, 0], X[y==0, 1], c='blue', alpha=0.5, label='Class 0', s=20)

axes[1].scatter(X[y==1, 0], X[y==1, 1], c='red', alpha=0.5, label='Class 1', s=20)

axes[1].contour(xx, yy, Z, levels=[0.5], colors='black', linewidths=2)

axes[1].set_title('Decision Boundary (black = 0.5 threshold)')

axes[1].legend()

axes[1].grid(True)

plt.tight_layout()

plt.show()Training accuracy: 0.9950

Final loss: 0.1523

8. Try It in the Browser¶

Adjust the learning rate and regularisation strength to observe how training converges.

import math

import random

random.seed(42)

def sigmoid(z):

return 1.0 / (1.0 + math.exp(-max(-500, min(500, z))))

n = 60

X = [random.gauss(-1, 1) for _ in range(n//2)] + [random.gauss(1, 1) for _ in range(n//2)]

y = [0] * (n//2) + [1] * (n//2)

lr = 0.5

lam = 0.01

w, b = 0.0, 0.0

for epoch in range(300):

grad_w, grad_b = 0.0, 0.0

loss = 0.0

for xi, yi in zip(X, y):

z = w * xi + b

yhat = sigmoid(z)

err = yhat - yi

grad_w += err * xi

grad_b += err

eps = 1e-15

loss -= yi * math.log(yhat + eps) + (1 - yi) * math.log(1 - yhat + eps)

w -= lr * (grad_w / n + lam * w / n)

b -= lr * grad_b / n

loss /= n

correct = sum(1 for xi, yi in zip(X, y) if (sigmoid(w*xi + b) >= 0.5) == bool(yi))

decision_boundary = -b / w if w != 0 else float('nan')

print(f'w = {w:.4f}, b = {b:.4f}')

print(f'Decision boundary: x = {decision_boundary:.4f}')

print(f'Training accuracy: {correct/n:.1%}')

print(f'Final loss: {loss:.4f}')9. Logistic Regression with scikit-learn¶

In practice use sklearn.linear_model.LogisticRegression. Note that sklearn’s C = 1/lambda — larger C means less regularisation.

%matplotlib inline

import numpy as np

import matplotlib.pyplot as plt

from sklearn.datasets import make_classification

from sklearn.linear_model import LogisticRegression as SklearnLR

from sklearn.model_selection import train_test_split

from sklearn.preprocessing import StandardScaler

from sklearn.metrics import accuracy_score, classification_report

X, y = make_classification(

n_samples=1000, n_features=5, n_informative=3,

n_redundant=1, random_state=42, class_sep=0.8

)

feature_names = ['monthly_charges', 'tenure', 'data_usage', 'support_calls', 'contract_length']

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=42)

scaler = StandardScaler()

X_train_s = scaler.fit_transform(X_train)

X_test_s = scaler.transform(X_test)

model_sk = SklearnLR(C=1.0, max_iter=1000, random_state=42)

model_sk.fit(X_train_s, y_train)

y_pred_sk = model_sk.predict(X_test_s)

print('Test accuracy:', accuracy_score(y_test, y_pred_sk))

print()

print(classification_report(y_test, y_pred_sk, target_names=['Stay', 'Churn']))

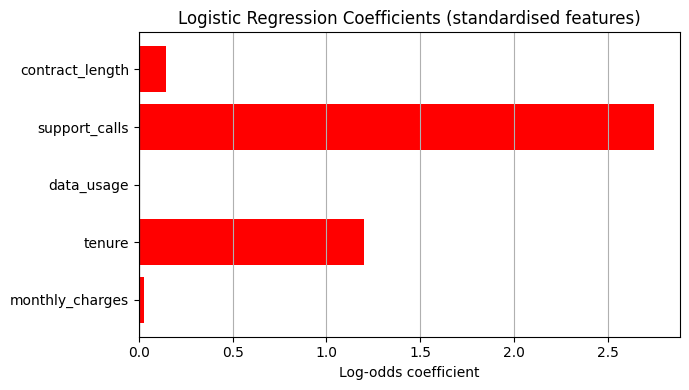

coefs = model_sk.coef_[0]

plt.figure(figsize=(7, 4))

colors = ['red' if c > 0 else 'steelblue' for c in coefs]

plt.barh(feature_names, coefs, color=colors)

plt.axvline(0, color='black', linewidth=0.8)

plt.xlabel('Log-odds coefficient')

plt.title('Logistic Regression Coefficients (standardised features)')

plt.grid(True, axis='x')

plt.tight_layout()

plt.show()

odds_ratios = np.exp(coefs)

print('\nOdds ratios:')

for name, OR in zip(feature_names, odds_ratios):

print(f' {name}: {OR:.3f}')Test accuracy: 0.875

precision recall f1-score support

Stay 0.80 0.95 0.87 87

Churn 0.96 0.81 0.88 113

accuracy 0.88 200

macro avg 0.88 0.88 0.87 200

weighted avg 0.89 0.88 0.88 200

/Volumes/MacSSD/01_Projects/Chandravesh-ML-Research/projects/jupyter-books/.venv/lib/python3.10/site-packages/sklearn/linear_model/_linear_loss.py:200: RuntimeWarning: divide by zero encountered in matmul

raw_prediction = X @ weights + intercept

/Volumes/MacSSD/01_Projects/Chandravesh-ML-Research/projects/jupyter-books/.venv/lib/python3.10/site-packages/sklearn/linear_model/_linear_loss.py:200: RuntimeWarning: overflow encountered in matmul

raw_prediction = X @ weights + intercept

/Volumes/MacSSD/01_Projects/Chandravesh-ML-Research/projects/jupyter-books/.venv/lib/python3.10/site-packages/sklearn/linear_model/_linear_loss.py:200: RuntimeWarning: invalid value encountered in matmul

raw_prediction = X @ weights + intercept

Odds ratios:

monthly_charges: 1.030

tenure: 3.318

data_usage: 1.006

support_calls: 15.614

contract_length: 1.153

10. Softmax Regression — Generalising to K Classes¶

For classes, the sigmoid is replaced by the softmax function:

The loss becomes categorical cross-entropy:

where is the one-hot indicator for class .

Connection to logistic regression: with , softmax reduces exactly to the sigmoid:

The gradient is also clean: — same error-times-feature structure.

%matplotlib inline

import numpy as np

from scipy.special import softmax

from sklearn.preprocessing import LabelBinarizer

from sklearn.datasets import load_iris

from sklearn.model_selection import train_test_split

from sklearn.preprocessing import StandardScaler

from sklearn.metrics import accuracy_score

class SoftmaxRegression:

def __init__(self, learning_rate=0.01, max_iter=1000, tol=1e-4, random_state=None):

self.learning_rate = learning_rate

self.max_iter = max_iter

self.tol = tol

self.random_state = random_state

self.weights = None

self.classes_ = None

self.bias = None

def _initialize_weights(self, n_features, n_classes):

if self.random_state is not None:

np.random.seed(self.random_state)

self.weights = np.random.randn(n_features, n_classes) * 0.01

self.bias = np.zeros(n_classes)

def _one_hot_encode(self, y):

self.label_binarizer = LabelBinarizer()

return self.label_binarizer.fit_transform(y)

def _gradient(self, X, y_true, y_pred):

error = y_pred - y_true

grad_weights = X.T @ error / X.shape[0]

grad_bias = np.mean(error, axis=0)

return grad_weights, grad_bias

def fit(self, X, y):

y_one_hot = self._one_hot_encode(y)

self.classes_ = self.label_binarizer.classes_

n_samples, n_features = X.shape

n_classes = y_one_hot.shape[1]

self._initialize_weights(n_features, n_classes)

prev_loss = float('inf')

for i in range(self.max_iter):

logits = X @ self.weights + self.bias

y_pred = softmax(logits, axis=1)

loss = -np.mean(np.sum(y_one_hot * np.log(y_pred + 1e-15), axis=1))

if np.abs(prev_loss - loss) < self.tol:

print(f'Converged at iteration {i}')

break

prev_loss = loss

grad_weights, grad_bias = self._gradient(X, y_one_hot, y_pred)

self.weights -= self.learning_rate * grad_weights

self.bias -= self.learning_rate * grad_bias

def predict_proba(self, X):

logits = X @ self.weights + self.bias

return softmax(logits, axis=1)

def predict(self, X):

return self.classes_[np.argmax(self.predict_proba(X), axis=1)]

iris = load_iris()

X_iris, y_iris = iris.data, iris.target

X_train_i, X_test_i, y_train_i, y_test_i = train_test_split(X_iris, y_iris, test_size=0.2, random_state=42)

scaler_i = StandardScaler()

X_train_i = scaler_i.fit_transform(X_train_i)

X_test_i = scaler_i.transform(X_test_i)

softmax_model = SoftmaxRegression(learning_rate=0.1, max_iter=2000, tol=1e-5, random_state=42)

softmax_model.fit(X_train_i, y_train_i)

y_pred_soft = softmax_model.predict(X_test_i)

print(f'Iris test accuracy: {accuracy_score(y_test_i, y_pred_soft):.4f}')Iris test accuracy: 1.0000

%matplotlib inline

import numpy as np

import matplotlib.pyplot as plt

from matplotlib.colors import ListedColormap

from sklearn.datasets import make_classification

from sklearn.linear_model import LogisticRegression

from sklearn.preprocessing import StandardScaler

def plot_decision_regions(X, y, model, resolution=0.02):

markers = ('s', 'x', 'o', '^', 'v')

colors = ('red', 'blue', 'lightgreen', 'gray', 'cyan')

cmap = ListedColormap(colors[:len(np.unique(y))])

x1_min, x1_max = X[:, 0].min() - 1, X[:, 0].max() + 1

x2_min, x2_max = X[:, 1].min() - 1, X[:, 1].max() + 1

xx1, xx2 = np.meshgrid(np.arange(x1_min, x1_max, resolution),

np.arange(x2_min, x2_max, resolution))

Z = model.predict(np.array([xx1.ravel(), xx2.ravel()]).T)

Z = Z.reshape(xx1.shape)

plt.contourf(xx1, xx2, Z, alpha=0.4, cmap=cmap)

plt.xlim(xx1.min(), xx1.max())

plt.ylim(xx2.min(), xx2.max())

for idx, cl in enumerate(np.unique(y)):

plt.scatter(x=X[y == cl, 0], y=X[y == cl, 1],

alpha=0.6, c=cmap(idx), edgecolor='black',

marker=markers[idx], label=cl)

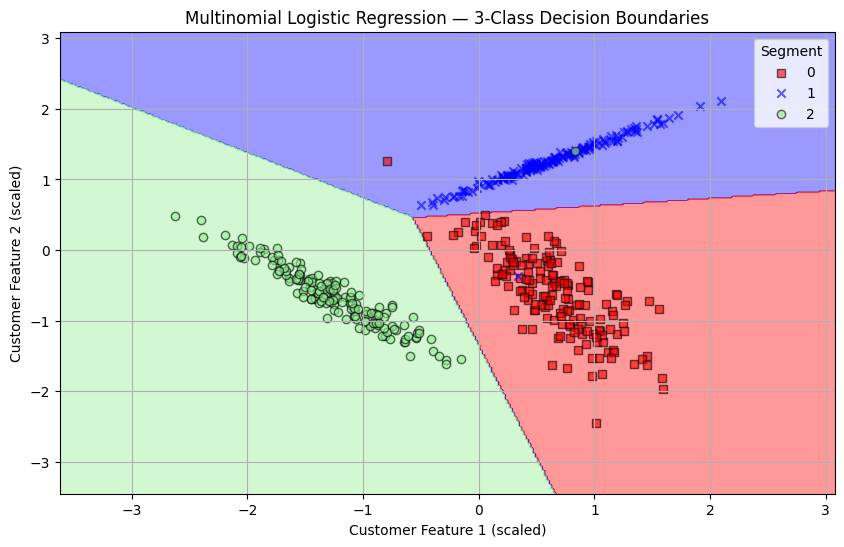

X_3, Y_3 = make_classification(

n_samples=500, n_features=2, n_redundant=0,

n_clusters_per_class=1, n_classes=3, class_sep=2.0, random_state=42

)

scaler_3 = StandardScaler()

X_3 = scaler_3.fit_transform(X_3)

logreg = LogisticRegression(C=1e5, multi_class='multinomial', solver='lbfgs')

logreg.fit(X_3, Y_3)

plt.figure(figsize=(10, 6))

plot_decision_regions(X_3, Y_3, logreg)

plt.xlabel('Customer Feature 1 (scaled)')

plt.ylabel('Customer Feature 2 (scaled)')

plt.title('Multinomial Logistic Regression — 3-Class Decision Boundaries')

plt.legend(title='Segment')

plt.grid(True)

plt.show()/Volumes/MacSSD/01_Projects/Chandravesh-ML-Research/projects/jupyter-books/.venv/lib/python3.10/site-packages/sklearn/linear_model/_logistic.py:1272: FutureWarning: 'multi_class' was deprecated in version 1.5 and will be removed in 1.8. From then on, it will always use 'multinomial'. Leave it to its default value to avoid this warning.

warnings.warn(

/Volumes/MacSSD/01_Projects/Chandravesh-ML-Research/projects/jupyter-books/.venv/lib/python3.10/site-packages/sklearn/utils/extmath.py:203: RuntimeWarning: divide by zero encountered in matmul

ret = a @ b

/Volumes/MacSSD/01_Projects/Chandravesh-ML-Research/projects/jupyter-books/.venv/lib/python3.10/site-packages/sklearn/utils/extmath.py:203: RuntimeWarning: overflow encountered in matmul

ret = a @ b

/Volumes/MacSSD/01_Projects/Chandravesh-ML-Research/projects/jupyter-books/.venv/lib/python3.10/site-packages/sklearn/utils/extmath.py:203: RuntimeWarning: invalid value encountered in matmul

ret = a @ b

/var/folders/93/7lt42x5j7m39kz7wxbcghvrm0000gn/T/ipykernel_68071/274246045.py:23: UserWarning: *c* argument looks like a single numeric RGB or RGBA sequence, which should be avoided as value-mapping will have precedence in case its length matches with *x* & *y*. Please use the *color* keyword-argument or provide a 2D array with a single row if you intend to specify the same RGB or RGBA value for all points.

plt.scatter(x=X[y == cl, 0], y=X[y == cl, 1],

/var/folders/93/7lt42x5j7m39kz7wxbcghvrm0000gn/T/ipykernel_68071/274246045.py:23: UserWarning: You passed a edgecolor/edgecolors ('black') for an unfilled marker ('x'). Matplotlib is ignoring the edgecolor in favor of the facecolor. This behavior may change in the future.

plt.scatter(x=X[y == cl, 0], y=X[y == cl, 1],

Knowledge Check¶

Why is logistic regression used for binary classification instead of plain linear regression?¶

What does the decision threshold do in logistic regression?¶

Minimising binary cross-entropy is equivalent to which statistical estimation principle?¶

If a logistic regression weight for feature x is theta = 0.693, the exponentiated odds ratio exp(theta) ≈ 2. What does this mean?¶

Exercises¶

Exercise 1 — Threshold Tuning¶

Using the LogisticRegression model trained on the churn dataset above, plot precision, recall, and F1 score as a function of threshold (sweep from 0.1 to 0.9 in steps of 0.05). Identify the threshold that maximises F1.

%matplotlib inline

# Exercise 1: threshold tuning

# Your code hereExercise 2 — Regularisation Strength¶

Sweep lambda_reg over [0.001, 0.01, 0.1, 1.0, 10.0] in your scratch LogisticRegression. For each value, fit on 80 % of the synthetic dataset and compute test accuracy. Plot accuracy vs log(lambda). At what lambda does the model start to underfit?

%matplotlib inline

# Exercise 2: regularisation sweep

# Your code hereCommon Pitfalls¶

Summary

The sigmoid maps a linear score to a valid probability.

Binary cross-entropy is the correct loss — convex, derived from MLE on Bernoulli labels.

The BCE gradient is — same structure as linear regression.

L2 regularisation = MAP with Gaussian prior;

C = 1/lambdain sklearn.Each coefficient is the log-odds change per unit feature; is the odds ratio.

Softmax regression generalises to K classes; with K=2 it reduces exactly to logistic regression.

Always scale features; watch for class imbalance and perfect separation.

What’s Next?¶

Logistic regression assumes features are roughly independent — it builds a single linear boundary. In Naive Bayes (naive_bayes.ipynb) we approach classification from a probabilistic generative model angle, explicitly modelling the class-conditional feature distributions and using Bayes’ theorem to derive the posterior.

Coming up in Chapter 7:

Naive Bayes — Bayes’ theorem, class-conditional independence, Gaussian vs Multinomial NB

Calibration & Class Imbalance — reliability diagrams, SMOTE, cost-sensitive learning

Classification Metrics — precision, recall, F1, AUC-ROC, AUC-PR

Lab — Churn Prediction end-to-end pipeline